Tree service insurance requirements are defined as the specific types and minimum levels of insurance coverage a tree care business must carry to operate legally, meet client contracts, and protect against financial loss. Every tree care business owner needs to understand what is tree service insurance requirement before signing a single contract or sending a crew to a job site. The core portfolio includes General Liability, Workers' Compensation, and Commercial Auto insurance, with additional policies added based on the scope of work. Clients ranging from homeowners to municipalities each impose their own standards, and a Certificate of Insurance (COI) is the document that proves compliance. Getting this wrong delays jobs and exposes your business to serious liability.

What are the essential insurance coverages required for tree service businesses?

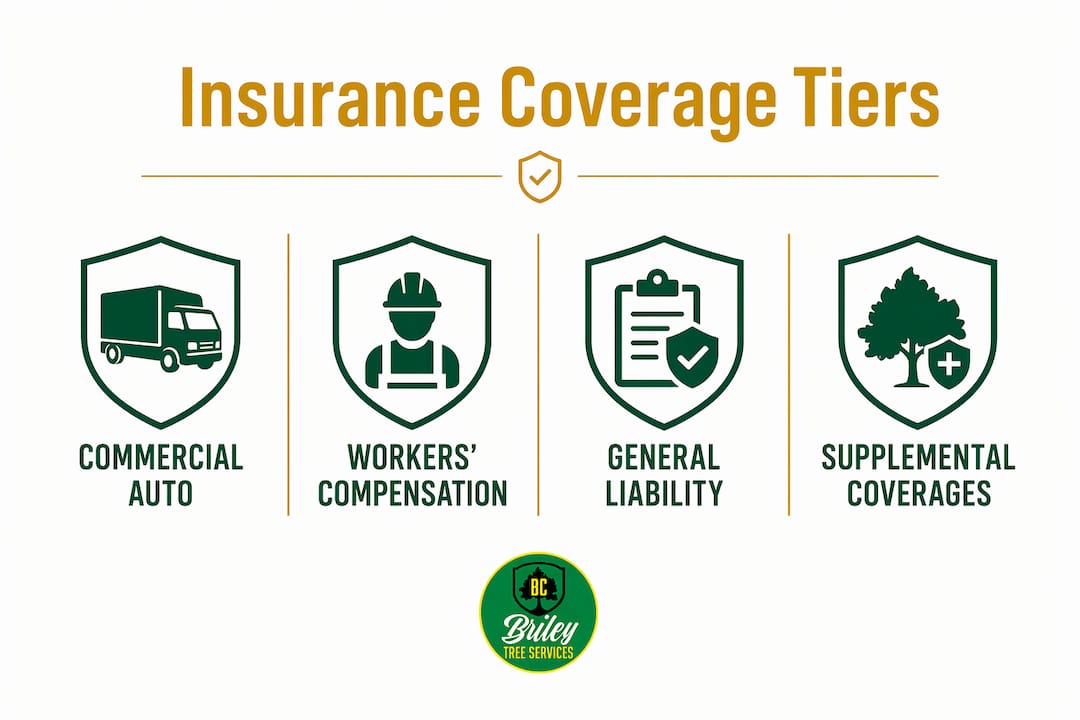

Tree service insurance basics start with four primary policy types, each covering a distinct category of risk. The combination you carry depends on your employees, vehicles, equipment, and the contracts you pursue.

General liability insurance

General Liability is the baseline coverage for any tree care operation. It protects against third-party injury and property damage claims arising from your work. A branch falls on a client's fence, or a crew member damages a parked car while chipping debris. Those claims go to your General Liability policy. Minimum limits often start at $1,000,000 per occurrence, though commercial and municipal clients frequently require $2,000,000 or more.

Workers' compensation insurance

Workers' Compensation is required by law in most states for any business with employees. It covers medical expenses and lost wages when a worker gets injured on the job. Tree work carries one of the highest injury rates of any trade, so this coverage is non-negotiable. Workers' comp is often contractually required even for sole proprietors when working for commercial clients, regardless of state law. Misclassifying workers or payroll categories directly affects your audit premiums, so accurate recordkeeping matters from day one.

Commercial auto insurance

Personal auto policies exclude business use. Commercial Auto covers trucks, trailers, and bucket trucks used in your operations. If a crew vehicle causes an accident on the way to a job site, a personal policy will deny the claim. Every vehicle your business owns or regularly uses needs to be listed on a Commercial Auto policy.

Supplemental coverages worth carrying

Some operations require policies beyond the core three:

- Inland Marine insurance covers equipment and tools while in transit or stored off-site. Chainsaws, rigging gear, and specialized climbing equipment are expensive to replace.

- Umbrella or Excess Liability extends your base coverage limits. High-exposure contracts such as crane operations or utility line work often require umbrella limits of $5,000,000 or more.

- Equipment Breakdown coverage protects against mechanical failure of owned machinery, which is separate from Inland Marine.

Pro Tip: Review your equipment coverage needs before bidding on any job that requires renting or transporting specialized machinery. A gap in Inland Marine coverage can leave you paying out of pocket for a $15,000 chipper.

How do client types and contracts affect tree service insurance requirements?

Insurance requirements depend heavily on who hires you and what the contract's risk transfer language says. The same tree removal job carries different insurance demands depending on whether the client is a homeowner, a property management company, or a city government.

Residential customers typically ask for basic proof of General Liability and Workers' Compensation. A COI naming them as the certificate holder is usually enough. The requirements are straightforward, and most standard policies satisfy them without modification.

Property managers and commercial clients add layers. They commonly require:

- Additional insured endorsements naming their company on your policy

- Primary and non-contributory language, meaning your policy pays first before theirs

- Waiver of subrogation, preventing your insurer from suing them after paying a claim

- Specific minimum limits, often $2,000,000 general aggregate or higher

Municipal and government contracts are the most demanding. Seattle, for example, requires $1,000,000 in Commercial General Liability with specific endorsements for any provider listed in its tree service registry. Many cities maintain similar registries with strict documentation requirements. Failing to match the exact endorsement language in the contract causes COI rejection and stops the job before it starts.

Pro Tip: Request the contract's insurance exhibit before your agent issues the COI. The exhibit lists the exact endorsements and certificate holder wording required. Sending a generic COI and hoping it matches is the most common reason tree service companies lose contract start dates.

Common pitfalls that cause COI rejection include wrong certificate holder names, missing endorsements, expired policy dates, and coverage limits that fall short of contract minimums. Each one requires your agent to reissue the COI, which takes time and creates friction with clients.

What is a Certificate of Insurance (COI) and why does it matter?

A COI is a standardized document issued by your insurance agent that proves your coverage is active. The COI lists insured parties, policy limits, effective dates, and required endorsements but does not create or modify the underlying policy. This distinction matters: a COI that lists an endorsement your policy does not actually carry is a compliance failure, not a fix.

The document your client receives contains these core elements:

- Named insured — the legal name of your business as it appears on the policy

- Certificate holder — the client or entity requesting proof of coverage

- Policy types and limits — General Liability, Workers' Comp, Commercial Auto, and any additional lines

- Effective and expiration dates — the active coverage period

- Description of operations — a brief statement describing the work covered

- Endorsements — additional insured, primary/non-contributory, waiver of subrogation, as required

COI endorsement details function as the controlling compliance checklist. Mere certificate issuance is insufficient without the correct endorsements and certificate holder names. A client's legal team will check every line.

| COI Element | Why It Matters |

|---|---|

| Named insured | Must match your legal business name exactly |

| Certificate holder | Must match the contract's required wording |

| Coverage limits | Must meet or exceed contract minimums |

| Endorsements | Must include all required policy modifications |

| Expiration date | Must cover the full project duration |

Inaccuracies on a COI create compliance gaps that can void coverage in a dispute. Work with your agent to build a COI template for each major client type. That reduces errors and speeds up issuance when a new contract comes in.

How to strategically manage insurance compliance for your tree care business

Proactive compliance management separates tree care businesses that win contracts from those that lose them on paperwork. Tree service insurance policies vary based on state, business structure, and job type, so a one-size-fits-all approach fails quickly.

Build your compliance process around these practices:

- Align your insurance portfolio with your contracts. Review every new contract's insurance exhibit before signing. If a contract requires coverage you do not carry, get it added before the job starts, not after.

- Classify payroll accurately. Accurately classifying payroll by job function is critical for workers' compensation audit accuracy and premium control. Ground crew, climbers, and office staff carry different class codes and rates.

- Manage subcontractor COIs proactively. Gaps in subcontractor coverage affect your own audit and liability exposure. Collect COIs before any subcontractor starts work, and track renewal dates so coverage does not lapse mid-project.

- Work with a specialist agent. General business insurance agents often miss arboriculture-specific risks. An agent who specializes in tree care understands class codes, high-risk operations, and the endorsement language your clients expect.

- Audit your COI library quarterly. Policies renew annually, but contracts run on different timelines. A COI issued in january may expire before a project ends in october.

Pro Tip: Build a simple spreadsheet tracking each client's COI requirements, the endorsements your policy carries, and the renewal dates. Cross-reference it every time you bid a new job. This single habit prevents most compliance delays.

Home service businesses in adjacent industries, including water damage restoration companies, face nearly identical COI and endorsement demands from insurance carriers and property managers. The compliance frameworks transfer directly to tree care operations.

Understanding emergency tree service contracts is equally relevant here, since storm response work often triggers the fastest and strictest insurance verification from property owners and adjusters.

Key Takeaways

Tree service insurance requirements are a portfolio of mandatory coverages, including General Liability, Workers' Compensation, and Commercial Auto, that must be matched precisely to each client's contract language and COI endorsement demands.

| Point | Details |

|---|---|

| Core coverage portfolio | Carry General Liability, Workers' Comp, and Commercial Auto as the baseline for any tree care operation. |

| Client type drives requirements | Residential, commercial, and municipal clients each impose different coverage limits and endorsement demands. |

| COI accuracy is non-negotiable | Every COI must match the contract's exact wording for certificate holder names and endorsements. |

| Payroll classification affects premiums | Accurate job-function classification controls workers' comp audit costs and prevents overpayment. |

| Subcontractor COIs create liability gaps | Collect and track subcontractor certificates before work starts to protect your own coverage. |

Why I think most tree care businesses get insurance compliance backward

Most tree care business owners treat insurance as a box to check after winning a contract. That approach costs real money and real jobs. I have seen crews show up to a site only to be turned away because the COI listed the wrong certificate holder name or was missing a waiver of subrogation. The client does not care that your coverage is solid. They care that the paperwork matches their contract.

The deeper issue is that most business owners do not read the insurance exhibit in a contract before signing. They sign, win the job, then hand the contract to their agent and hope the existing policy covers it. It often does not. Commercial and municipal clients write their insurance requirements to protect themselves, not you. The additional insured endorsement, the primary and non-contributory language, the waiver of subrogation — each one shifts financial risk onto your policy. You need to understand what you are agreeing to before you agree to it.

Working with an agent who specializes in arboriculture makes a measurable difference. A specialist knows that a climber and a ground worker carry different workers' comp class codes. They know that crane operations require umbrella limits most general agents never think to ask about. That expertise saves money at audit time and prevents coverage gaps that a general agent would never catch.

My honest advice: treat your COI library as a living document, not a file you forget about after issuance. Review it every quarter. Match it against your active contracts. Fix mismatches before a client finds them.

— Tatum

Brileytreeservice: professional, insured tree care in Shreveport

Brileytreeservice operates as a fully insured tree care company serving Shreveport, Bossier City, and Northwest Louisiana. Every job, from tree removal and trimming to stump grinding and emergency storm cleanup, is backed by proper coverage and professional documentation. Residential and commercial property owners across the Shreveport area rely on Brileytreeservice because the team shows up prepared, works safely, and cleans up completely. For property managers and commercial clients who require proof of insurance before work begins, Brileytreeservice provides the documentation you need without delay. Contact Brileytreeservice today for a free estimate on any tree care service.

FAQ

What insurance do tree services need to operate legally?

Tree service businesses need General Liability, Workers' Compensation, and Commercial Auto insurance at minimum. Additional policies such as Inland Marine and Umbrella Liability are required for higher-risk or commercial contracts.

How much does tree service insurance cost?

Costs vary based on payroll size, coverage limits, state requirements, and the types of work performed. There is no single published rate; get quotes from agents who specialize in arboriculture to get accurate pricing for your operation.

What is a Certificate of Insurance for tree services?

A COI is a document issued by your insurance agent that proves your coverage is active. It lists policy limits, effective dates, named insured, and any endorsements required by the client's contract.

Do tree service companies need additional insured endorsements?

Commercial and municipal clients almost always require additional insured endorsements. Endorsement details including primary and non-contributory status and waiver of subrogation are contractually mandated and must appear on the COI exactly as specified.

How do tree service insurance requirements change for government contracts?

Government contracts impose the strictest requirements, including specific coverage limits and mandatory endorsements. Seattle's tree service provider registry, for example, requires $1,000,000 in Commercial General Liability with named endorsements before a provider can be listed.